Advanced Parameters

From the 27th of December 2021, FactSet source will be completely replaced and will be no longer available.

For any issue you may encounter, please refer to our recommendations and workaround. For more information about this process please follow our guidelines and information.

General Settings Parameters

Keyword | Description | Value | |

|---|---|---|---|

| historical | Historical fundamental. | |

forecast | Estimates. | ||

| Specifies the data provider. | WVB | WVB (historical fundamental). |

MRS | Morning Star (historical fundamental). | ||

SNP | S&P (historical estimates). | ||

| Infront | Infront data source (estimates). | ||

AUTO (default) | Infront Analytics’s best source (see help center for rules explanation). | ||

Specifies the output currency. | Reference (default) | The currency used by the company when reporting its financial statements. | |

EUR | |||

USD | |||

… | |||

| Specifies a specific date. For more information, see Period and Reference Date Settings Tables. | YYYYMMDD | A date between 1/1/1900 and 31/12/2999 in a valid ISO date format. Can be used only in conjunction with "referencePeriod" to build NTM, or LTM rolling 12 months period. |

Today | Refers to today’s date. Can be used to refer to a relative date. | ||

Yesterday | Refers to yesterday's date. Can be used to refer to a relative date. | ||

CWS | Current Week Start (always a Monday). Can be used to a relative date. | ||

CMS | Current Month Start. Can be used to refer to a relative date. | ||

CYS | Current Year Start for the 1st January of the current year. Can be used to refer to a relative date. | ||

referencePeriod | Specifies a specific period. For more information, see Period and Reference Date Settings Tables. | YYYY | A year between 1900 and 2999. |

| LASTY | Last available company year (historical). Can be used to refer to a relative date. | ||

| LTM | Last Twelve Months (historical). Use the company interim report to provide fresh yearly data. | ||

| NTM | Next Twelve Months (forecast). Refers to the immediate next twelve months from the current date. | ||

| CY | Current Year (current calendar year if the current date is after 3rd of July, and the previous calendar year otherwise). Can be used to refer to a relative date. | ||

| LASTINT | Last available company interim (historical + interim). | ||

| FY-1 | Previous Forecast year (equivalent to CY-1 and DatasetType is forecast). | ||

| FY0 | Forecast year 0 (equivalent to CY and DatasetType is forecast). | ||

| FY1 / FY2 / FY3 | Forecast year 1, 2 or 3 (equivalent to CY+1, +2 or +3 and DatasetType is forecast). | ||

| 2019:S1 or 2019:S2 | First or second semester of 2019. | ||

| 2018:Q1 or Q2, Q3, Q4 | First, second, third or fourth quarter of 2018. | ||

Does not apply on items such as open, high, low, close. Please note that you can set the default value from the Infront Excel Add-In settings, "Functions Module" menu, default values panel. | U K (default) M B | Convert in unit. Convert in thousands. Convert in millions. Convert in billions. | |

| n | The number n of decimals. The default value is set to 4 decimals. | |

| Applies only to time series items such as open, high, low, close, volume, market capitalization. | n | The number n of days to go backward to find a point. The default value is set to 35 days. |

Specific Parameters

Some parameters are available for some specific fields, as beta calculation or unlevered beta.

Beta is often used as a risk measurement or as a WACC calculation (Weighted average cost of capital).

Beta is a statistics indicator that compare the evolution of the company’s series to another series, generally an index representing a country or a region. The comparison of the stock evolution to the market index evolution.

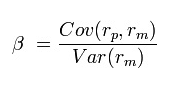

Formula:

The beta's calculation is the covariance between the stock return and the index return, divided by the variance of the index (over a period of 3 years for example).

The beta value is calculated based on the historical returns of a share relative to an index. The beta coefficient will therefore depend on three variables: (1) the number of periods over which we estimate our covariance / variance relationship (1 year, 3 years, 5 years), (2) the frequency of the data (daily, weekly, monthly, yearly) and (3) the benchmark index (S&P, NASDAQ, Dow Jones, CAC40 ...).

Therefore, for the calculation, 3 parameters are needed:

| Keyword | Description | Value | |

|---|---|---|---|

| Specifies the index to choose to compare the company. | Country | Local index (set by default). |

Regional | Regional index. | ||

ADX | ADX index. | ||

CAC 40… | CAC 40 index. | ||

| The frequency is typically used weekly or monthly. | Daily | The frequency is set by default to weekly. |

| Weekly | |||

| Monthly | |||

| To have a meaningful result, we need a minimum to 6-months to 1-year calculation. A minimum period of 3 years is recommended if the frequency is set to monthly. | n-days | The number n of days / weeks / months or years. Set to 1 year by default. |

| n-weeks | |||

| n-months | |||

| n-years | |||

For more information, please watch a quick video about INFGET() advanced parameters.